Weekly Bond Market Report, Friday March 13, 2026

Ten Cuts Deep: Kenya's Central Bank Bets on Growth

Market Overview

During the week ended 13th March 2026, the market showed a slow performance in the bond market, equities, derivatives, Eurobonds and the international market.

International oil prices remained volatile during the week with Murban crude oil trading at USD 92.13 per barrel on March 12, compared to USD 76.25 per barrel on the previous week led by the ongoing US-Iran conflicts.

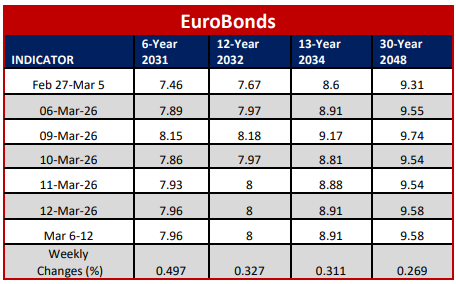

Yields on Kenya’s Eurobond increased for a forth consecutive week by 33.37 basis point during the week. The Eurobonds performed generally well in most countries in Africa.

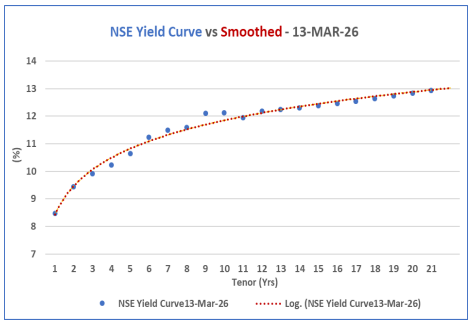

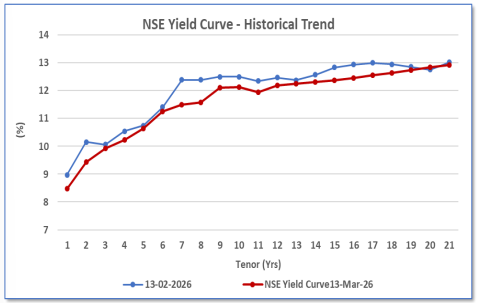

The NSE yield curve has generally edged downwards in the medium-term end 5 to 8 -year horizon while remaining relatively stable in the short-term and a relative shooting at the long term, partially influenced by the CBR rate cut, Iran war and the inflation decline.

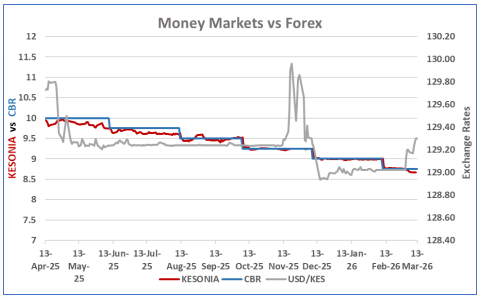

The Kenya Shilling remained relatively stable against major international and regional currencies during the week ending March 13th, 2026. It exchanged at KES 129.23 per U.S. dollar on average over the past week edging upwards compared to previous week.

The Monetary Policy Committee (MPC) Lowered for the 10th consecutive series, the Central Bank Rate (CBR) to 8.75% from 9.00% . This observes the 25 basis point rate cut trend.

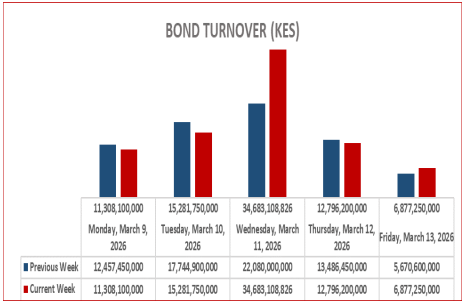

Bond turnover in the domestic secondary market ROSE over the week by 13.30% closing at 80.9 billion.

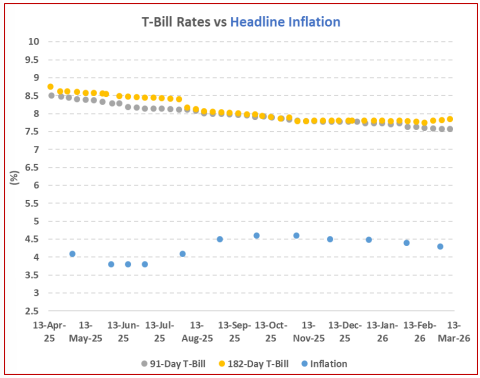

The Kenyan inflation lowered to 4.3% in February from 4.4% in January. This shows stability of the economy and the market. Most core and non-core items prices declined leading to the inflation decline. However expected to rise due to the middle East conflicts.

Interest Rate Outlook

Money Market Trends

The Kenya Shilling remained relatively stable for the past weeks with no aggressive fluctuations, most specifically against the US dollar.

On average the Kenyan Currency against the USD exchanged at KES 129.15 over the week.

KESONIA remained stable at 8.74 on average over the week ending Friday, 13th March 2026.

Central Bank Rate (CBR) dropped to 8.75% from 9.00% following the Monetary Policy Committee (MPC) meeting held early February. The rate cut will results to lower lending rates amongst many factors.

Short End of the Yield Curve and Inflation Trends

This week saw T-bills oversubscribed for the seventh consecutive time, with a subscription rate of 182.3%, down from 418.4% the previous week.

The 91-day T-bill attracted bids totaling KES 5.0 billion against KES 4.0 B offered, resulting in a subscription rate of 124.5%. Conversely, the subscription rates for the 182-day and 364-day papers declined to 78.9% and 308.7%, respectively.

The government accepted KES 32.3 billion of the KES 43.7 billion bids received, achieving a 73.8% acceptance rate.

Yields showed mixed results, with the 182-day paper yield slightly increasing to 7.8%, the 364-day paper yield declined to 8.5%, and the 91-day paper yield remaining stable at 7.6%.

The Kenyan inflation lowered to 4.3% from 4.4% in January. This shows stability of the economy and the market. Most core and non-core items prices declined leading to the decline.

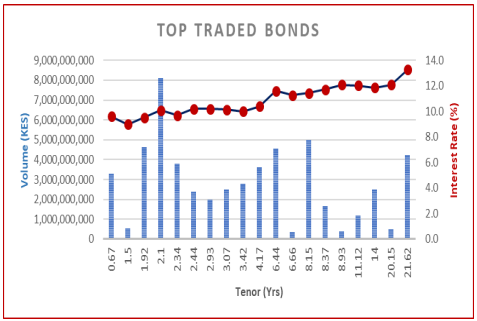

Kenya Secondary Bond Market Trends

The NSE yield curve has generally edged downwards in the medium -term end 5 to 12 -year horizon while relatively shooting in the short -term and long- term papers.

The curves shows extreme performance before and after the CBR rates change early this months and the inflation decline.

Week-on-week traded volumes have generally been aggressive across the two week period with turnover shifting within the week, the turnover ROSE with a margin of 13.30% for the week ended 13th Mar 2026 compared to the previous week.

The turnover closed at 80.95 Billion for the week.

Kenya Primary Bond Market

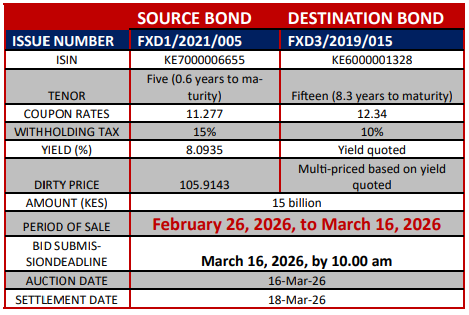

Treasury Bond Switch

The Kenyan Central Bank has announced a plan to convert KES 15 billion worth of short-dated Treasury bond into longer-tenor bond.

From FXD1/2021/005 - 0.6 Years Remaining with 11.2770% coupon Maturing in November 9, 2026 to FXD3/2019/015 - 8.3 Years Remaining with a 12.3400% coupon rate which matures On July 10, 2034.

Important dates:

Sale period: February 26–March 16, 2026

Date of auction: March 16, 2026

Date of settlement: March 18, 2026

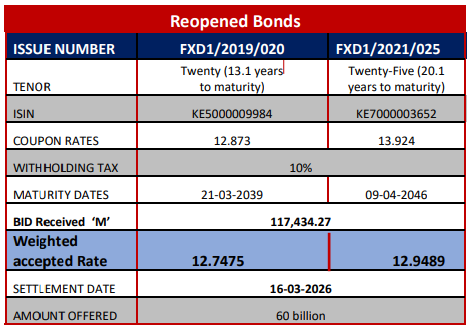

Treasury Bond Auctions

During the week, the Central Bank of Kenya announced the results of its auction for the reopened treasury bonds FXD1/2019/020 and FXD1/2021/025, which have tenors of 13.1 and 20.1 years, with fixed coupon rates of 12.9% and 13.9%.

The auction was oversubscribed at a rate of 195.7%, garnering bids worth KES 117.4 billion against KES 60.0 billion offered.

The government accepted KES 61.0 billion in bids, achieving an acceptance rate of 51.9%, with weighted average yields of 12.7% and 12.9%, lower than previous levels from prior auctions in January and December 2025.

With February 2026 inflation at 4.3%, real returns stand at 8.4% and 8.6%, while tax-equivalent yields for the bonds are 13.5% and 13.7%, respectively, after factoring in withholding taxes.

International Bond Markets

U.S. Treasury yields surged amid inflation concerns, with the 10-year yield rising to around 4.27% as oil prices exceeded $100 per barrel and worries about fiscal deficits increased.

In the UK, gilt yields climbed due to weak growth and energy price shocks, while the government successfully issued a Green Gilt.

German Bund yields also rose in response to expected ECB tightening, influenced by higher energy prices.

Japan saw modest increases in JGB yields amidst a weaker yen, while China's bond market remained stable, focusing on macro data within an accommodative policy stance by the People Bank of China.

Kenya Eurobond Market

Yields on Kenya’s Eurobonds performed slightly lower this week compared to previous week.

On average, yields increased by 33.37 Basis points. This suggests some upward price movement or balancing by investors in response to global market conditions amidst geopolitical wars.

In attachment, is the performance of the Daily Eurobond turnover for the week ended 13th March 2026 in statistical way.

Bulletin Board

Nation Media Group Acquisition

Proposed Indirect Acquisition of Stake in Nation Media Group; On 10 March 2026, Taarifa Ltd announced a proposed indirect acquisition of 54.08% of the issued shares in Nation Media Group PLC from Aga Khan Fund for Economic Development S.A.

The Tanzanian Business Man Rostam Azizi issued a briefing on the planned acquisition and confirmed the proceedings.

EABL Change of Mantle

EABL Appoints New Group CFO Designate; East African Breweries PLC announced the appointment of Justin Molloy as Group Chief Financial Officer Designate, effective 1 May 2026. He will succeed the current CFO starting 1 July 2026.

Justin is currently the Finance Director of Diageo Ireland where he has built a reputation for delivering business growth strategies, managing complex financial operations and continuously transforming processes for business success.

Kenya Forex Reserves

Kenya's forex reserves fell by USD 136M this week to USD 14.46B, equivalent to 6.2 months of import cover.

Remittances

Remittances from Kenya's diaspora increased to $412.7M in February 2026, up $30.5M YoY (+7.98%) from $382.2M in February 2025 but down $14.7M MoM (-3.4%) from $427.4M in January 2026.

With inflows remaining over $400 million, the gain reverses a three-month YoY fall in November 2025 (-8.2%), December 2025 (-2.2%), and January 2026 (-0.3%).

Centum Complete Sale in Sidian Bank

Centum Completes Sale of Stake in Sidian Bank; Centum Investment Company PLC announced the completion of the sale of its entire stake in Bakki Holdco Limited, which previously served as the holding vehicle for its interest in Sidian Bank Limited.

Through Bakki Holdco, Centum indirectly held 27.2% of Sidian Bank, with Centum owning 50% of Bakki Holdco.